(原标题:巴菲特《我最看好的股票》的6个选股要点!)

巴菲特因为格雷厄姆开始研究GEICO,并买入,之后在GEICO经历危机时以极低的价格吸到了血筹码,最后全面收购了GEICO。

GEICO是格雷厄姆这辈子收益最大的股票,但这个股票为什么好,一直以为自己懂了,但今天看了老李哥分享给我的文章《我最看好的股票》,这是巴菲特20岁时(1951)写的文章,20岁他就深谙了选股的关键,而我在20岁时还什么都不懂!

具体文章可见:《我最看好的股票》

The nature of the industry is such as to ease cyclical bumps. The majority of purchasers regards auto insurance as a necessity.

汽車保險產業本身具有平滑週期性波動的特點。大部分汽車購買者都認為車險是有必要的。

Industry advantages include lack of inventory, collection, labor and raw material problems. The hazard of product obsolescence and related equipment obsolescence is also absent.

這個產業的優勢還包括沒有存貨、收款、勞動力和原材料等方面的問題,而且也沒有產品過時和相關設備被淘汰的風險。

The term “growth company” has been applied with abandon during the past few years to companies whose sales increases represented little more than inflation of prices and general easing of business competition.

“成長型企業”一般是指那些剔除物價上漲和商業競爭緩和的因素,過去幾年銷售依然有所成長的企業。

(当然过去的增长不能说明未来也能增长,所以需要预判未来是否有增长潜力,GEICO市占率还有望进一步提升)

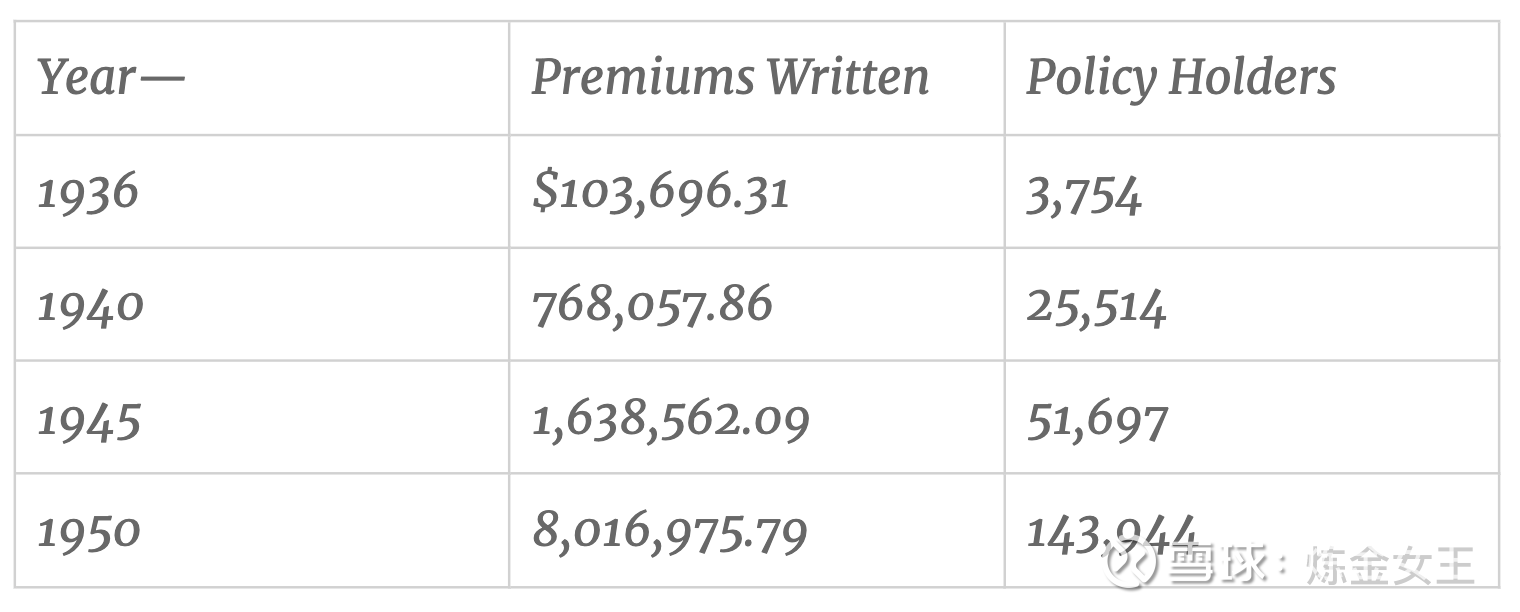

Probably the biggest attraction of GEICO is the profit margin advantage it enjoys. The ratio of underwriting profit to premiums earned in 1949 was 27.5% for GEICO as compared to 3.7% for the 135 stock casualty and surety companies summarized by Best’s. As experience turned for the worse in 1950, Best’s aggregate’s profit margin dropped to 3.0% and GEICO’s dropped to 13.0%.

GEICO最大的吸引力也許來自於它的利潤率。1949年公司保險利潤與保費收入的比率為 27.5%,而 Best’s的135家事故保險公司平均利潤率僅為6.7%。1950年景氣轉差,Best’s計算的平均利潤率降至3%,而GEICO降至18%。

另外,补充一下,GEICO本身针对的人群安全系数更高,而且没有中间商,成本优势明显。

At the end of 1950, the 10 members of the Board of Directors owned approximately one third of the outstanding stock.

截至1950年末,董事會10位董事共持有GEICO流通股的三分之一左右。

(小公司内部人士持股率低,大概率说明两个点,一是没有那么看好公司;二是没有经营好企业的动力!)

At the present price of about eight times the earnings of 1950, a poor year for the industry, it appears that no price is being paid for the tremendous growth potential of the company.

以目前股價來看,當前估值為1950年 (產業景氣糟糕年份) 盈利的8倍,看起來完全沒有反映公司巨大的成長潛力。

@大股市小书虫 @ericwarn丁宁 @鱼香基丝 @流浪行星 @LoveKonan

首页

首页 微信公众号

微信公众号

证券之星APP

证券之星APP